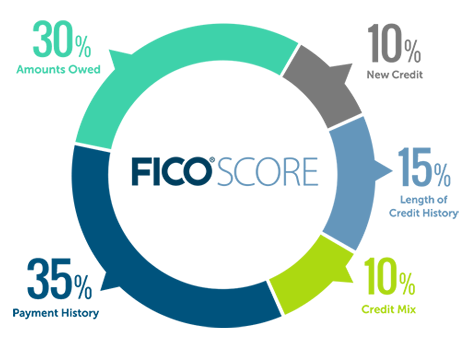

One of the ongoing complaints about FICO is an alleged lack of transparency of their

scoring systems. This has lead to many complaints not only directly to FICO, but now

to the newly formed Consumer Financial Protection Bureau or CFPB. In February 2012

the Occupy Wall Street Alternative Banking movement sent an open letter to Richard

Cordray, Director of the CFPB with some pretty strange and radical suggestions.

First and foremost, Occupy Wall Street (hereafter “OWS”) has asked the CFPB to

“centrally manage the credit scoring system” rather than allowing the credit reporting

agencies to do so. This suggestion, while fairly absurd, suggests that the credit

reporting agencies manage the credit scoring system, which they don’t. FICO is the

developer of the software that calculates the FICO scores. The credit bureaus are

simply licensed to sell FICO scores based on their data.

OWS is also suggesting, “Credit scores should be calculated using a model that is public

and freely available.” That seems like a fair request, until you actually think about what

that means. First off, most consumers have no clue what their FICO scores are. This

would make any public accessibility of the FICO scoring model meaningless. Second,

and perhaps more importantly, the FICO scoring model is a proprietary product built

by FICO, the publically traded company. The company makes hundreds of millions of

dollars a year because of the sale of their scores. Making their scoring models (and

the countless other types of credit scoring models used by financial service, utility, and

insurance companies) would expose the intellectual property to anyone and everyone.

That seems incredibly unfair to the companies (and there are many more than just

FICO) that build credit scoring systems and depend on their sale to maintain operations,

which includes employing tens of thousands of people worldwide. And while I realize

this is an overused analogy, requiring FICO to make their models public and freely

available is really no different than requiring Coca-Cola, Kentucky Fried Chicken, and

every other company who has developed a unique brand and product to simply give

away their trade secrets.

They are also suggesting “Credit reports sent to consumers, including those sent

pursuant to the free annual credit report available to consumers under current law,

should always contain the consumers numeric credit score.” This has been an ongoing

complaint about FACTA, which is the law that gives consumers the right to get their

credit reports once every 12 months from the credit bureaus. In fact, it was debated

prior to the passage of FACTA whether credit scores should also be disclosed. The

current language of the Fair Credit Reporting Act does not require the disclosure of

credit scores.

There are many issues regarding adding credit scores to the required disclosure of

credit reports. First, it seems that consumers aren’t really that interested in getting

copies of their credit reports pursuant to the Federal rules. A little less than 4% of the

Federally mandated free credit reports are claimed each year. That’s not indicative of

strong consumer demand and there’s nothing suggesting that simply adding a score

to the disclosure would increase the take rate. Additionally, the credit bureaus would

not disclose a consumer’s FICO score if they were forced to include some number on a

credit report.

The credit bureaus have made it evident that they do not want to further the FICO brand

and they would likely disclose either the VantageScore or one of their other home grown

scores, like the PLUS score from Experian or the TransRisk score from TransUnion or

the ERS score from Equifax. The problem is that none of the aforementioned scores

has any market share comparable to FICO. PLUS isn’t even commercially available to

lenders.

This one is one of my favorites; “There should be a way for an individual to forecast how

his or her credit score would change under various circumstances – e.g., if he/she paid

their electric bill late, had a different credit card balance, etc.” If the OWS folks would

spend about 10 seconds on the Internet they’d find a variety of free score simulator tools

that do exactly what they’re asking the CFPB to force the credit bureaus to do.

And next, “There should be due process for disputes over negative credit information.”

I guess the OWS folks aren’t familiar with the Fair Credit Reporting Act, which

clearly defines the credit bureau’s and data furnisher’s obligations as it relates to any

information in dispute. You may disagree that the current process is a good process, but

you can’t argue that there isn’t a process already well established.

And finally, “Credit scores should be tied to individuals and should not be imputed to

spouses.” Again, the OWS folks are showing a lack of understanding about how credit

reports are maintained by the credit reporting agencies. Credit reports, the sole basis for

credit scores, are not merged at the credit repository level when you get married. You

always have individual credit reports. And because you always have individual credit

reports you will always have individual credit scores. So, that request has already been

fulfilled without the need for CFPB intervention.

“The Credit Guru”, Longtime FICO Insider & Credit Industry Authority President Of The Ulzheimer Group, LLC

John Ulzheimer is a nationally recognized expert on credit reporting, credit scoring and identity theft. He is the President of The Ulzheimer Group, the Director of Credit Education at DisputeSuite.com, Credit Expert at CreditSesame.com and the credit blogger for Mint.com. Formerly of FICO, Equifax and Credit.com, John is the only recognized credit expert who actually comes from the credit industry. He has served as a credit expert witness in more than 150 cases and has been qualified to testify in both Federal and State court on the topic of consumer credit.

DisputeSuite is provides a variety of solutions for your credit repair business. From engaging custom websites to dispute processing services to a robust CRM with automations and portals, DisputeSuite has everything you need for your credit repair business. Register here to join us weekly to hear industry updates, expert speakers and business tips & tricks!